Since our investment activity began in 2011, we have been steadily growing our investment portfolio each year. By 2026, SCF will have a portfolio of 11 investments worth $6 million.

Prototype micro-lending program using a flexible underwriting system designed to fund early-stage low-income businesses.

Status:Inactive

# of Investments: 1

Investment Term: 2015-2019

Loan Amount: $200,000

Area Served: Alabama, Texas, Louisiana, Mississippi, Kentucky, Tennessee

In 2015, SCF loaned $200,000 to support LiftFund’s Promise Loan Program. This prototype micro-lending program incorporated a unique underwriting system designed to fund early-stage low-income business owners that LiftFund’s existing programs were not previously able to serve. After 3-4 years of testing and revising the program to overcome high losses, LiftFund tightened its underwriting criteria to reduce Promise Loan defaults. Consequently, SCF’s capital was not being adequately deployed to end-users due to the tightened lending standards and resulting lower deployments overall. SCF’s loan to LiftFund was subsequently modified in October 2017 to allow its funds to support the newer LiftUp loan program. LiftUp loans were developed to serve clientele similar to the Promise Loan program but by utilizing LiftFund’s standard underwriting parameters (these standards had been loosened on some important criteria based on learnings gained from the Promise Loan Program).

LiftFund

Texas Growth Market Loans

Loans to low-income small businesses in a region targeted for growth.

Status:Inactive

# of Investments: 4

Investment Term: 2011-2014

Loan Amount: $25,000-$27,318

Area Served: San Antonio, Texas

SCF’s $27,000 loan supported low-income business owners in San Antonio, Texas, allowing LiftFund to increase its lending capacity in a well-established market region with unmet loan capital needs. SCF selected LiftFund (previously Accion Texas, Inc.) given it status as a U.S. small business microloan industry leader. Our capital was targeted to grow LiftFund’s lending within its historic and to expand to new geographic markets, as well as to continue serving low-income, minority, and underserved populations. LiftFund’s borrowers are typically low-income small-business owners, of which over 80% were minorities and 35% were women (at the time of investment).

Loans to low-income small businesses owners in new expansion markets in the state.

Status:Inactive

# of Investments: 4

Investment Term: 2011-2014

Loan Amount: $40,000-$43,709

Area Served: New Orleans, Shreveport, and Alexandria, Louisiana

SCF’s $44,000 loan increased small-business loans to low-income owners in New Orleans, Shreveport, and Alexandria, Louisiana. These were new expansion regions for LiftFund where there existed unmet lending needs. SCF selected LiftFund (previously Accion Texas, Inc.) given its status as a U.S. small business microloan industry leader. Our capital was targeted to grow LiftFund’s lending within its historic and to expand to new geographic markets, as well as to continue serving low-income, minority, and underserved populations. LiftFund’s borrowers are typically low-income small-business owners, of which over 80% were minorities and 35% were women (at the time of investment).

MercyCorps Northwest

Small Business Loan Fund

Microloans to low-income small-business owners within the Pacific Northwest.

Status:Inactive

# of Investments: 1

Investment Term: 2016-2020

Loan Amount: $120,000

Area Served: Seattle, WA; Portland, OR

MercyCorps Northwest (MCNW) programs work to increase economic self-sufficiency and community integration through microenterprise development and self-employment. MCNW assists low-income, current and aspiring small-business owners throughout Oregon and Washington in order to reduce unemployment, grow personal incomes and assets, and increase economic growth. MCNW provides high-touch technical assistance to prepare prospect borrowers to launch and grow their businesses before and after their loans of under $50,000 are disbursed. SCF invested in MCNW by targeting to grow its loan fund to serve more low-income clients and to support its efforts to expand its service area, especially within its newer Seattle region.

Native American Bancorporation

Native American Bank Business Loans

Loans supporting under-resourced Native American entrepreneurs and community/economic development projects across 22 states.

Status:Inactive

# of Investments: 1

Investment Term: 2018-2022

Loan Amount: $300,000

Area Served: National; Focus on Native Americans and Tribal Areas

SCF invested in NAB’s holding company (Native American Bancorp) because NAB is part of a small but important list of mission-oriented banks—it is one of only 18 Native banks and the only one with a national footprint. NAB is a Native CDFI and a Minority Depository Institution because of its cooperative ownership by over 30 tribal nations/entities. NAB’s pursuit of diversifying native economies and creating sustainable communities in rural poor regions is of critical importance. SCF’s loan to NAB provides them with growth capital to achieve their 5-year strategic growth goals. Importantly, SCF’s $300,000 investment into the holding company allows for these funds to be leveraged 1:11 which opens the opportunity for NAB to raise an additional $3.3M, thus greatly increasing their overall lending capacity.

Loans paired with CDBG business loans for low-to-moderate income small businesses in rural upstate Michigan.

Status:Active

# of Investments: 2

Investment Term: 2014-2030

Loan Amount: $75,000-$500,000

Area Served: 12 counties in rural Upper Michigan

SCF provided Northern Initiatives (NI), a CDFI, with a loan to support its new Regional Revolving Loan Fund program (RRLF) in Michigan. The RRLF lends to low-to-moderate income small-business owners in upstate rural Michigan. Funds from this investment are coupled with approximately $4.25 million in Community Development Block Grant Program (CDBG) funds from 12 rural Michigan counties. CDBG is a federal government sponsored program designed to provide low-to-moderate income people and businesses with funds to support various economic and community development activities. The pairing of SCF funds with CDBG funds provides NI with greater flexibility to deploy loans. SCF’s funds are able to be used for loan activities that are needed by the borrowers to achieve success but excluded by CDBG loan parameters. NI’s overall investment portfolio consists of 40% women-owned businesses, 60% microloans, and 20% start-up businesses.

Northern Great Lakes Initiatives

New Markets Expansion Capital

Loans for women, minority and veteran entrepreneurs in lower-Michigan expansion region.

Status:Inactive

# of Investments: 1

Investment Term: 2019-2025

Loan Amount: $300,000

Area Served: Southern Michigan

This capital supports NI’s small business lending activities targeting “diverse” populations—women, minorities, and veterans—within NI’s more recent service expansion areas within lower Michigan’s rural and minor urban areas. The loans funded will be capped at $60,000 in order to target to serve small and emerging businesses—a sector that has been largely underserved, and even more so as it relates to women and minorities. As part of its efforts to increase its lending to more diverse populations, NI will incorporate flexible underwriting criteria, heightened outreach efforts (including opening new offices), develop language and culturally appropriate materials. NI also anticipates that it will need to provide these new entrepreneurs with higher levels of training and business technical assistance services in order for them to achieve stability, growth and success.

Oikocredit USA

Oikocredit International Micro-Loan Fund

Loans to Oikocredit’s partner microfinance, farming cooperatives and social enterprises serving the lowest income populations across the world.

Status:Inactive

# of Investments: 1

Investment Term: 2015-2016

Loan Amount: $150,000

Area Served: International /Developing Countries

SCF’s investment in this US-based capital-raising arm of Oikocredit International provided general funding for Oikocredit International to grow its development financing and technical assistance to its 800+ partner organizations—microfinance institutions, fair trade co-ops, renewable energy initiatives and social enterprises—in over 60+ developing countries in Africa, Asia, Latin America and the Caribbean.

Runway Project

The Runway Project - Oakland

Loans for early-stage businesses run by African Americans that use non-traditional underwriting and offers holistic business support.

Status:Inactive

# of Investments: 1

Investment Term: 2017-2022

Loan Amount: $100,000

Area Served: San Francisco – East Bay Area

Runway Project Oakland is part of a national initiative solving the “Friends & Family” seed funding gap for African American entrepreneurs. This program strives to fix the broken infrastructure surrounding African American entrepreneurs. It provides early-stage funding using a flexible underwriting process and holistic high-touch business support. Loans are low-interest and capped at $20,000. Runway Project builds and leverages a connected ecosystem of funders and business service providers as a wealth-building strategy for the entrepreneur. Core partners in the Oakland-based prototype program include: Self Help Federal Credit Union, Impact Hub Oakland, Uptima and other entrepreneur bootcamps. Between the launch of the program in October 2017 and December 31, 2019, twenty one loans had been made to African American entrepreneurs and additional capital is also being raised to continue to grow this investment fund.

Multi-use loans to low-to-moderate income borrowers in 6 states across the USA.

Status:Active

# of Investments: 7

Investment Term: 2015-2026

Loan Amount: $100,000-$330,000

Area Served: California, Illinois, Wisconsin, Washington, South Carolina, Connecticut

SCF made an initial $250,000 Certificate of Deposit investment into the Self Help Federal Credit Union (SHFCU) general loan fund.The loans include auto, unsecured, and mortgage loans as well as affordable consumer loans like Dreamer, Citizenship and Just Right loans. Traditionally, loans from SHFCU have been distributed to 86% low-income borrowers, 93% to people of color, 33% to women; 63% of all loans have been made into distressed areas. The geographic scope of SHFCU’s lending has greatly expanded and loans are now being deployed within California, Illinois and Florida. As a CDFI, SHFCU has positioned itself as a national leader in providing financial services to low-income and underserved populations.

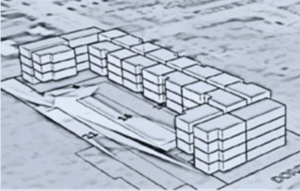

The Fifty Five

Fifty-Five Apartments

A loan to fund the site acquisition to develop 60 units of affordable multi-family housing (30-80% AMI) with 7,500 SF commercial space in Atlanta, Georgia.

Status:Active

# of Investments: 1

Investment Term: 2024 – 2025

Loan Amount: $650,000

Area Served: Atlanta, Georgia

The Fifty-Five is a four-story mixed-use complex being developed by Gorman & Company. It incorporates 60 affordable apartments ranging from one to three bedrooms, all reserved for households earning between 30%-80% of area median income. The project also includes 7,500 square feet of ground-floor commercial space. Located in East Point, Fulton County GA, on a 1.25-acre site, the project will also incorporate amenities, such as outdoor community gathering areas, a gym, and a computer center. As Atlanta’s economy grows and housing costs continue to rise, Fifty-Five Apartments will see that the community’s low-income residents have access to affordable quality housing options. SCF’s investment provided part of the project’s land loan to acquire the project site.